The economic crisis began in November 1997 as international creditors rushed to withdraw their loans to domestic banks. The BOK provided emergency lending to banks, but could not meet the escalating demand for foreign currency. The foreign exchange reserve was quickly depleted and an explosive devaluation followed.

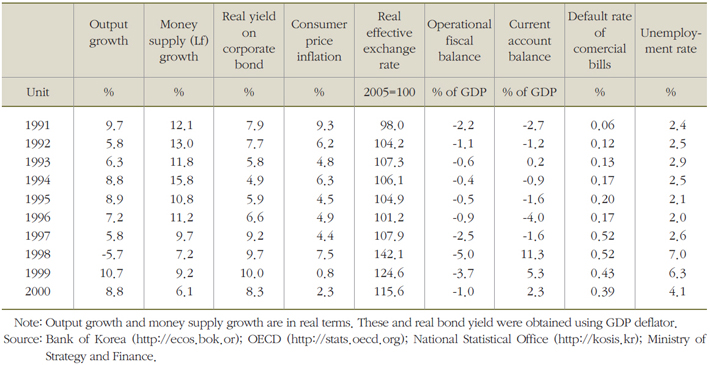

Before the outbreak of the crisis, it was difficult to spot abnormalities in major macroeconomic indicators (Table 2-15). Output growth, money supply, interest rate, inflation, exchange rate and fiscal balance were all at their trend levels. The only signs of instability came from the external sector. The current account deficit surged to 4.0 percent of GDP in 1996 due to the terms-of-trade shock generated by plummeting semiconductor prices. Total external liabilities increased by 27 percent per year between 1992 and 1996 to reach 163.3 billion dollars. Of particular importance was the increase in short-term external liabilities that corresponded to 280 percent of the foreign exchange reserve in 1996. Most of the increase could be explained by foreign currency borrowing by financial institutions.

Table 2-15. Major macroeconomic indicators (1991-2000)

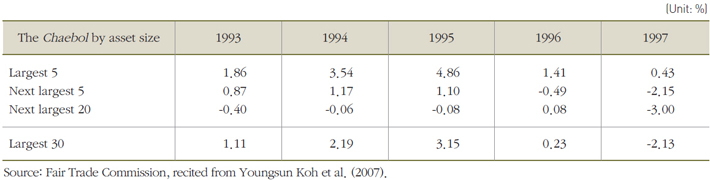

Given the poor risk management, financial institutions became increasingly vulnerable to external shocks. The insufficiency of data makes it difficult to gauge the depth of the problem, but Hahm and Mishkin (2000) estimate that non-performing loans in 1996 made up 22 percent of the total financial credit to the corporate sector. This reflected the low profitability of businesses (Table 2-16). The largest 30 chaebol recorded an average return on assets (ROA) of 0.2 and -2.1 percent in 1996 and 1997, respectively. In early 1997, some chaebol went bankrupt and the general shortage in liquidity began to afflict businesses.

Table 2-16. Average return on assets of the largest 30 chaebol

Instability increased in international financial markets as well. Thailand and other Southeast Asian countries came near to a foreign exchange crisis in August 1997. Asian stock markets crashed in October, and worries spread to Japan’s financial markets. International credit rating agencies began to downgrade Korea, which was finally engulfed in the financial crisis at the end of November.

Many explanations have been suggested for the financial crisis. They can be categorized broadly into two schools, with one finding the root cause in the economic fundamentals of the country in crisis and the other emphasizing the self-fulfilling nature of the crisis. According to the first, weak economic fundamentals-inconsistency between exchange rate policy and other policies (monetary and fiscal policy in particular), financial weakness of the corporate and banking sector, implicit state guarantees to businesses and financial institutions, and unsustainable current account deficits-are at the heart of any foreign exchange crisis. In the case of East Asian countries, the unhealthy relationship between government and the private sector (so-called “crony capitalism”) produced widespread weaknesses in the economy. International investors, sensing these weaknesses, began to pull capital out of the country and the crisis erupted.

In contrast, the second school maintains that international financial markets demonstrate a high degree of intrinsic instability. When every creditor expects other creditors to withdraw from acountry, there will occur a “run” on the country, driving down the currency and generating bankruptcies. A collective action of this sort can ruin a country even if its fundamentals are sound. According to Radelet and Sachs (1998), the sharp rebound of the East Asian countries after the crisis indicates that their problem lay not in insolvency arising from weak fundamentals, but illiquidity produced by international creditors’uncoordinated withdrawal. Korea, for example, could come out of the turmoil only after foreign creditor banks collectively agreed to the rollover of short-term debts.

There is not enough clear-cut evidence to support either of these two opposing views, which implies that both may contain some degree of truth. Accordingly, the policy response of the Korean government was centered on (1) restructuring corporate and financial sectors to redress fundamental weaknesses and (2) seeking international help to tide over the illiquidity. The following subsection dwells on policy responses after the crisis.

Source : SaKong, Il and Koh, Youngsun, 2010. The Korean Economy Six Decades of Growth and Development. Seoul: Korea Development Institute.