Financial liberalization proceeded very slowly in the 1980s and early 1990s. In the early 1980s, the real interest rate turned positive as inflation stabilized, providing a favorable environment for interest rate reform. The large amount of corporate debt, however, precluded active liberalization because even a slight rise in interest rates would increase interest payments substantially. A partial liberalization was tried in 1984 and 1986 without noticeable impact. A more ambitious plan was announced in December 1988, but revoked in early 1989 when the interest rate jumped due to price instability.

The next round of interest rate reform was embodied in the Four-Stage Interest Rate Liberalization Plan announced in August 1991. The Plan proposed liberalization to move from long-term to short-term interest rates, from securities market rates to bank interest rates, and from large-sum to small-sum instruments. The actual liberalization, however, was not guided by this principle. Full implementation was also delayed for years; liberalization began officially in the latter half of 1991 but was completed only in 1996-1997 (Yoon Je Cho, 2003, pp.85-86; OECD, 1996, p.48).

Directed credits also continued. In 1982, the government consolidated the less important credit programs into a general credit program and reduced interest subsidies significantly. But at the same time, it expanded credit programs for small- and medium-sized enterprises (SMEs). The minimum share of SMEs in banks’ lending portfolio was raised in 1980, and this regulation was extended to non-bank financial institutions (NBFIs) in 1985. The BOK began to provide are discount facility in 1983 to various types of SME loans by DMBs, and strengthened support in the mid-1980s and thereafter. As a result, the total amount of directed credits decreased very slowly (Joon-kyung Kim, 1993, pp.131-134).

The BOK’s involvement in directed credits was not limited to SME support. As explained above, the BOK supplied 1,722.1 billion won of cash to banks during the industrial rationalization in 1985-1987. It also released 250.0 billion won to agricultural, fisheries and livestock cooperatives in 1987 as part of a debt-relief program for farmers and fishermen. In 1992, three investment trust companies received 2,900.0 billion won from the BOK. These companies had been ordered by the government to buy stocks to support the collapsing market. The attempt failed and they incurred enormous losses, which the government tried to make up for through BOK lending (Pyung-joo Kim, 1995).

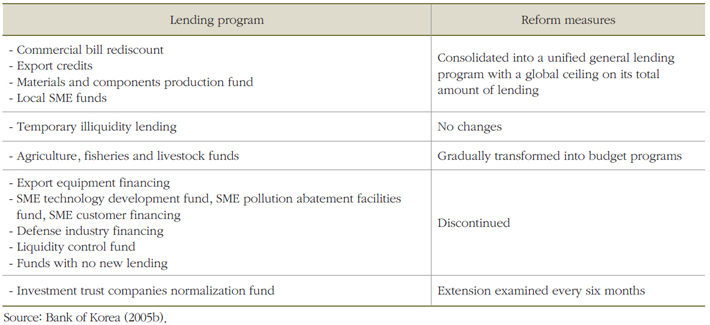

Criticism of BOK lending grew. In response, the government set out to streamline BOK lending programs and reduce their size in 1994 (Table 2-11). Of particular importance were the abolition of automatic rediscounting and the consolidation of various programs into a unified lending program with a global ceiling on its total amount of lending. The ceiling was to be determined ex ante. This arrangement allowed greater room for maneuver for the BOK (Bank of Korea, 2005b, p.97).

Table 2-11. Reform of BOK lending programs (March 14, 1994)

There was a wave of privatization of commercial banks in the early 1980s. In addition to the one that had been already privatized in 1973, four others were privatized between 1981 and 1983. 1) Government intervention continued, however, in the operation of the privatized banks, such as management appointments, asset management and organizational changes. Government influence on the nomination of bank presidents was abolished officially in 1993, but political influence remained (OECD, 1996, p.43; Yoon Je Cho, 2003, p.94).

The 1980s and early 1990s also witnessed the entry (and sometimes exit) of many banks and NBFIs. Forerunners of NBFIs included finance companies 2) and merchant banking corporations (MBCs) 3) that had been in place since the 1970s. A host of other NBFIs such as mutual savings banks, life insurance companies, investment trust companies, securities companies, investment advisory companies, venture capital companies and lease companies also sprang up. NBFIs were subjected to lighter regulations than banks because they had been created in the first place to siphon off funds from unorganized financial markets into organized ones. Their lending and deposit rates were higher than bank rates, restrictions on asset portfolio were fewer, market entry was easier, and directed credit was not an obligation. In particular, many chaebol acquired control over NBFIs and lobbied, often successfully, for further deregulation. These enabled NBFIs to grow rapidly in the 1980s (Yoon Je Cho, 2003, p.94).

Banks lost their market share to NBFIs continuously until the mid-1980s. Recognizing the disadvantages faced by banks, the government allowed them to undertake trust business through special accounts (“trust accounts”) classed with non-bank intermediaries. Trust accounts grew rapidly in volume afterwards, and their share in total domestic liabilities of DMBs rose from 5 percent in 1984 to over 40 percent in 1993 (OECD, 1994, pp.102-103).

In 1993, the government liberalized the interest rate on commercial papers (CPs) and permitted bank trust accounts to be invested in CPs. In addition, the ceiling on the share of securities in the asset portfolios of trust accounts was also raised from 40 to 60 percent. These changes led to a very rapid expansion of the CP market. The share of CPs in total corporate financing rose from 2.5 percent in 1990-1992 to 13.1 percent in 1993-1996, and peaked at 17.5 percent in 1997. Companies preferred CPs to bank credits because banks normally required detailed project plans before making loans to large projects whereas the underwriters of CPs did not require such plans as long as companies received an eligible rating from credit rating agencies (Yoon Je Cho, 2003, p.96).

The constant creation, conversion, merger and diversification of banks and NBFIs was adesirable phenomenon from the perspective of financial liberalization. The instability of the financial system, however, increased with liberalization as prudential regulation was not strengthened simultaneously. The problems with prudential regulation at the time can be summarized as follows.

First, the amount of loans that were not subject to prudential regulation grew as the CP market and the bank trust accounts expanded. For instance, bank loans from the general account were subject to a regulation that limited the amount of loans to a single borrower, whereas the same loans from the trust account was not subject to a similar regulation (Yoon Je Cho, 2003, p.87).

Second, regulatory standards remained outdated. Before the 1997 crisis, the prudential regulation of banks was based on the Management Improvement Measure, something similar to the prompt corrective action adopted after the crisis. The Measure, however, had many weaknesses; the criteria to identify problem banks were complicated; the conditions to take corrective actions were neither objective nor transparent; it was left to the authorities’ discretion whether to take action or not; and the authorities could not close down troubled banks (Won-hyeong Choi, 1996). As for NBFIs, supervision was practically non-existent due to the absence of a regulatory framework (such as a capital adequacy ratio) and insufficient regulatory efforts by the MOF. Some MBCs were even found after the crisis to have engaged in fraudulent operations (Inseok Shin and Joon-Ho Hahm, 1998 p.28).

Third, various authorities were involved in prudential regulation, creating overlaps and gaps in supervision. The Office of Bank Supervision (OBS) within the BOK was in charge of the banking sector, and the Ministry of Finance (MOF) most of the NBFI sectors. Within the banking sector, general accounts were supervised by the OBS, whereas trust accounts by the MOF. The BOK was concerned mostly with the banks’ compliance with a list of credit allocation guidelines set by the government and less with the assessment of their risk exposure and the prevention of excess risk-taking. The MOF did not have the manpower and expertise to carry out proper supervision of financial institutions (Yoon Je Cho, 2003, p.95).

Fourth, the authorities did not pay sufficient attention to the strengthening of the financial market infrastructure necessary for the sound operation of amarket-based financial system. Accounting and disclosure standards remained unchanged, and the credit rating capacity was not enhanced (Yoon Je Cho, 2003, p.96).

To summarize, financial market became increasingly liberalized in the 1980s and early 1990s, especially as many chaebol, as owners of NBFIs, demanded deregulation. The liberalization, however, lacked a clear orientation and was not accompanied by a concurrent strengthening of prudential regulation. A fundamental reform was delayed because politicians and bureaucrats were not ready to bear the short-term costs. Enforcing prudential regulation would have required the restructuring of many businesses and financial institutions.4) This would have helped clarify the respective responsibilities of the state, businesses and financial institutions and dismantle the risk partnerships among them, but no effort was made in this direction. Phillip Wonhyuk Lim (2001, p.15) portrays the situation as “de-control without de-protection,” with the state giving up directing the economy while still willing to insure risks. A well-planned action by the government to “de-protect” the corporate and financial sector would have made the crisis of 1997 significantly less painful, if not preventing it

Source : SaKong, Il and Koh, Youngsun, 2010. The Korean Economy Six Decades of Growth and Development. Seoul: Korea Development Institute.

NOTE

1) Korea Commercial Bank (1973), Hanil Bank (1981), Korea First Bank and Seoul Trust Bank (1982), and Choheung Bank (1983).

2) Finance companies were first introduced in the money market after the August 3rd Measure of 1972. They were involved mainly in discounting and trading commercial papers. Twelve new finance companies were added in the aftermath of two large-scale money market frauds in 1982-1983, and their number totaled 32 in 1990. But the worsening business environment in ensuing years forced their conversion into other types of NBFIs. Five of them were converted into securities companies and three into banks in 1991, and the rest into MBCs in 1994 (nine) and 1996 (fifteen).

3) An MBC is a mixture of the British merchant bank and the American investment bank with an added function of medium- to long-term equipment lending. MBCs were created after the first oil shock to help domestic companies tap into foreign capital markets, but their remit covered domestic markets in commercial papers, securities and corporate bonds as well. There existed six MBCs until the early 1990s. With the subsequent conversion of 24 finance companies into MBCs, their number increased to 30 by 1997. After the economic crisis, however, 29 MBCs were either closed or merged, while one new MBC was established, leaving two MBCs in the market.

4) As noted above, the interest rate reform was delayed for the same reason.

References

· Cho, Yoon Je,“ The Political Economy of Financial Liberalization in South Korea,”in Chung H. Lee (ed.), Financial Liberalization and the Economic Crisis in Asia, Routledge Curzon, 2003, pp.82-103.

· OECD, OECD Economic Surveys: Korea, 1996.

· Kim, Joon-kyung, “Improving the Funding of Policy Loans,”in Daehee Song (ed.), National Budget and Policy Objectives, Research Monograph 93-03, Korea Development Institute, 1993, pp.114-176 (in Korean).

· Kim, Pyung-joo, “Financial Institutions and Economic Policies,”in Dong-Se Cha and Kwang Suk Kim (eds.), The Korean Economy 1945-1995: Performance and Vision for the 21st Century, Korea Development Institute, 1995, pp.179-254 (in Korean).

· Bank of Korea, Monetary Policy in Korea, 2005b (in Korean).

· OECD, OECD Economic Surveys: Korea, 1994.

· Choi, Won-hyeong, “Prompt Corrective Actions for a Sound Management of Banks,”Monthly Bulletin, Bank of Korea, June 1996, pp.3-22 (in Korean).

· Shin, Inseok and Joon-Ho Hahm, “The Korean Crisis-Causes and Resolution,”KDI Working Paper, No. 9805, Korea Development Institute, 1998.

· Lim, Phillip Wonhyuk, “The Evolution of Korea’s Development Paradigm: Old Legacies and Emerging Trends in the Post-Crisis Era,”ADB Institute Working Paper, No. 21, July 2001.