The global financial crisis that started with the fall in housing prices in the United States in 2007 became truly global in scale as Lehman Brothers filed for bankruptcy in September 2008. In Korea, output shrank by 4.5 percent in the fourth quarter of 2008 (17 percent in annual terms). Even before the global financial crisis, there had been small and large shocks in the 2000s, such as the collapse of the KOSDAQ market in 2000 after the burst of IT bubble and the credit card crisis in 2003. But these shocks arose from domestic sources 1) and did not result from a global economic downturn.

The American economy, the epicenter of the crisis, has had structural problems for years. Blanchard (2009) points to four such problems 54 2) (1) the assets that were created and traded appeared much less risky than they truly were; (2) securitization led to complex and hard-to-value assets being placed on the balance sheets of financial institutions; (3) securitization and globalization led to increasing connectedness both within and across countries; and (4) leverage increased. These problems produced asset price bubbles and increased the vulnerability of financial system.

The global crisis threw Korean financial markets into disarray. The sudden capital outflow caused a severe credit crunch in the domestic financial market. The stock market plunged by 40.7 percent in the course of 2008 and declined further by 5.5 percent in the first two months of 2009. Domestic banks faced serious difficulties in rolling over foreign debt. The won weakened by 40 percent against the dollar between October 2008 and February 2009.

The American economy, the epicenter of the crisis, has had structural problems for years. Blanchard (2009) points to four such problems 54 2) (1) the assets that were created and traded appeared much less risky than they truly were; (2) securitization led to complex and hard-to-value assets being placed on the balance sheets of financial institutions; (3) securitization and globalization led to increasing connectedness both within and across countries; and (4) leverage increased. These problems produced asset price bubbles and increased the vulnerability of financial system.

The global crisis threw Korean financial markets into disarray. The sudden capital outflow caused a severe credit crunch in the domestic financial market. The stock market plunged by 40.7 percent in the course of 2008 and declined further by 5.5 percent in the first two months of 2009. Domestic banks faced serious difficulties in rolling over foreign debt. The won weakened by 40 percent against the dollar between October 2008 and February 2009.

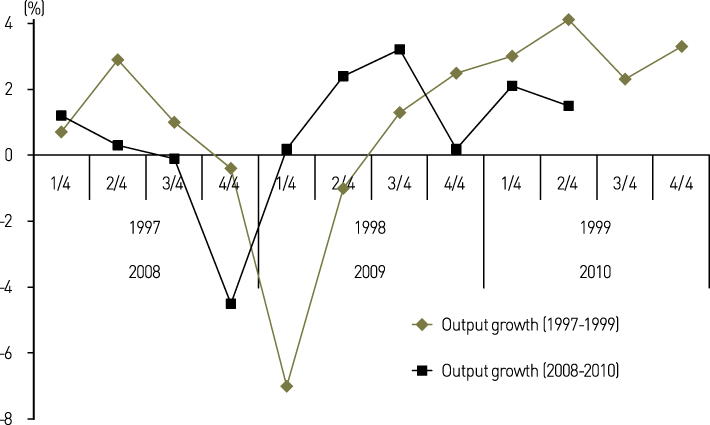

Figure 2-18. Output growth Comparison of 1997-1999 and 2008-2010

The industrial sector was also battered by the precipitous fall in exports and investment.

In the last quarter of 2008, exports contracted by 41 percent, investment by 45 percent, and output by 17 percent in annual terms. Still, the pain was milder than during the 1997 crisis; output returned to positive growth in the first quarter of 2009 (Figure 2-18).

The rapid recovery from the crisis was due to, among other reasons, the reduced vulnerability of the financial and corporate sectors as a result of the restructuring following the 1997 crisis; the reduction of home equity loans before the 2008 crisis due to various regulations; and prompt policy responses to the crisis. The policy responses can be summarized as follows.

First, the government and BOK provided 55 billion dollars in foreign currency (21 billion dollars in export credits and 34 billion dollars in emergency liquidity) to the banking sector between October 2008 and February 2009. It also announced that state guarantees would be provided for new foreign borrowing by domestic banks and their overseas branches until June 2009. In October 2008, the BOK and the Federal Reserve signed a currency swap accord worth 30 billion dollars. In December, similar swap accords were arranged with Japan and China, each worth 30 billion dollars. These measures, together with the current account surplus, helped to ease the shortage in foreign liquidity; the rollover rate of banks’ foreign borrowing dropped to around 50 percent in October but recovered to 106 percent in March 2009.

Second, the BOK slashed its policy rate from 5.25 to 2 percent between September 2008 and February 2009. It also rapidly expanded domestic liquidity by 23 trillion won through purchases of RPs (repurchase agreements) and treasury bonds and early repayment of MSBs.

Third, fiscal policy took an expansionary turn. On top of the tax cuts announced before the crisis, the government introduced asupplementary budget in September 2008 to increase spending. Total spending growth in 2008 was 14 percent, well above the 5-10 percent observed in previous years. Spending was further increased in 2009 by 14 percent.

As a result, the operational fiscal balance recorded adeficit of 4 percent of GDP in 2009.

Fourth, the government announced a plan to expand credit guarantees for SMEs through various public funds. All expiring guarantees during 2009 would be automatically extended, the hurdle for borrowers would be lowered to get new guarantees, and the guarantee ratio would be raised from 85 to 100 percent of the loan amount for some types of borrowers (e.g., exporting companies).

Fifth, the burden of home equity loans was lessened for borrowers. They could get guarantees equivalent to the decline in their housing prices up to 100 million won. The maximum grace period and repayment period of home equity loans were extended to 5-10 years and 30-35 years, respectively. Those who wanted to move from variable to fixed interest payments were exempted from associated fees.

Sixth, recapitalization schemes were prepared to strengthen the financial health of financial institutions and to facilitate the corporate sector restructuring. In the first round, the Bank Recapitalization Fund, worth 20 trillion won, was set up with capital injections of 10, 2, and 8 trillion won from the BOK, KDB and institutional investors, respectively. In the second round, the Financial Stabilization Fund was set up within the Korea Finance Corporation, a state-owned financial institution specializing in policy loans, to support the recapitalization of banks and NBFIs. In addition, a Restructuring Fund worth 40 trillion won was set up within the Korea Asset Management Corporation to buy and dispose of impaired asset owned by financial institutions and restructured enterprises.

Source : SaKong, Il and Koh, Youngsun, 2010. The Korean Economy Six Decades of Growth and Development. Seoul: Korea Development Institute.

NOTE

1) The KOSDAQ market collapse in 2000 was attributed to the low interest rate maintained since late 1998 to stimulate recovery.The credit card crisis in 2003 was also attributed to the low interest rate maintained after the IT bubble burst and the September 11 attacks. Another cause of the credit card crisis was the moral hazard of credit card companies that took advantage of deregulation to rapidly expand their operations, and the lack of appropriate responses by the regulatory authorities.

2) The following discussion draws from Joon-kyung Kim (2009)