The giddy output growth of 9 percent in the 1970s was accompanied by macroeconomic imbalances (Kwang Suk Kim and Joon-kyung Kim, 1995, p.66). Excess demand created by the HCI drive, the Middle East construction boom and fiscal deficits, combined with the first and second oil shocks, produced a rapid escalation in inflation. A delay in devaluation1) amid high inflation led to the overvaluation of won and the loss of price competitiveness of Korean exports. Exports shrank in 1979 for the first time since the early 1960s. Output growth turned negative in 1980 due to a crop failure and political instability following the assassination of President Park.

The need for change was initially brought up within Park’s administration. Since early 1978, the staff of the Economic Planning Board (EPB), together with economists at the Korea Development Institute (KDI), studied the problems affecting the Korean economy and made strenuous efforts to persuade the president to adopt a stabilization program (Heung-ki Kim, 1999, p.276). The result was the Comprehensive Economic Stabilization Program announced in April 1979.

The Program touched on the most sacred parts of the administration’s policy agenda, and proposed reducing export subsidies, moderating HCI investments, and scaling back the rural housing improvement program. It also proposed liberalizing prices and interest rates, which was unthinkable at the time.

It encountered fierce opposition from other ministries and the president himself ordered the continuation of export subsidies. Nonetheless, stabilization came to take center stage in economic policy, and the successor administration of Chun Doo-hwan adopted “stability” and “private sector-led growth” as its slogan. These changes were reflected in the fifth Five-Year Plan (1982-1986). 2)

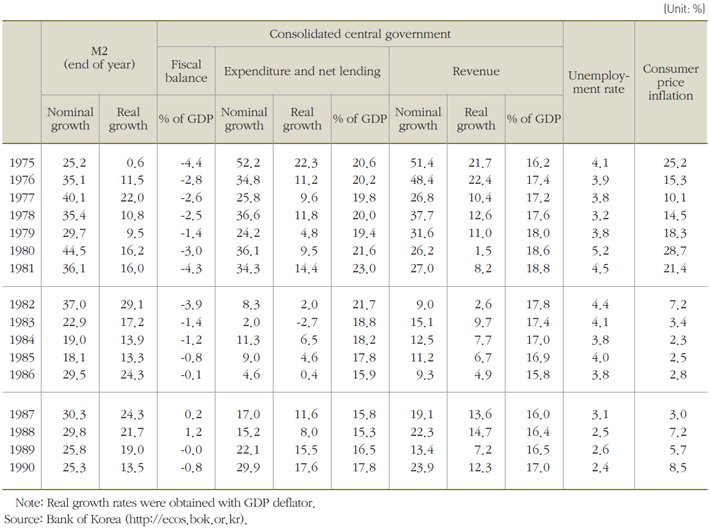

Stabilization was pursued with monetary and fiscal contractions. The annual M2 growth declined from 35 percent in 1975-1982 to 20 percent in 1983-1985 (Table 2-9). But the decline was mostly a passive response to the slowdown in inflation; the real growth rate actually rose slightly from 13 to 14 percent. What contributed more to price stabilization was moderation in rice price increases and active fiscal consolidation.

In 1981, the rice price paid by the government to farmers was set at 14 percent above the previous year’s price, far below the level demanded by the opposition party (45.6 percent) or the Ministry of Agriculture and Fisheries (at least 24 percent). The incident demonstrated the government’s commitment to stabilization (Heung-ki Kim, 1999, p.289; Economic Planning Board, 1994, p.109).

In 1982, the government introduced zero-based budgeting (ZBB) 3) and cut the budget that was already being implemented. In addition, the 1983 budget was prepared with great restraint; the central government’s consolidated spending decreased by 2.7 percent in real terms in 1983 (Table 2-9). Fiscal consolidation continued through 1986 and successfully curbed spending growth. The fiscal balance improved markedly; a deficit of -4.3 percent of GDP in 1981 turned into a surplus of 0.2 percent in 1987.

Fiscal consolidation, together with the stabilization of oil prices, helped consumer price inflation to drop from over 20 percent in 1981 to under 5 percent in 1983. Inflation has remained below 10 percent ever since.

Table 2-9. Major macroeconomic indicators (1975-1990)

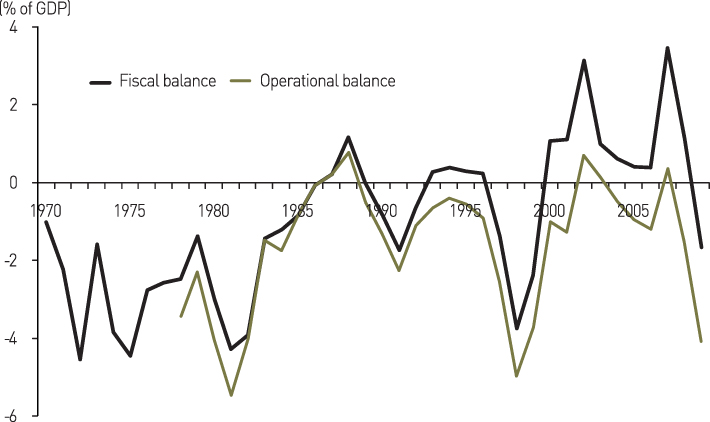

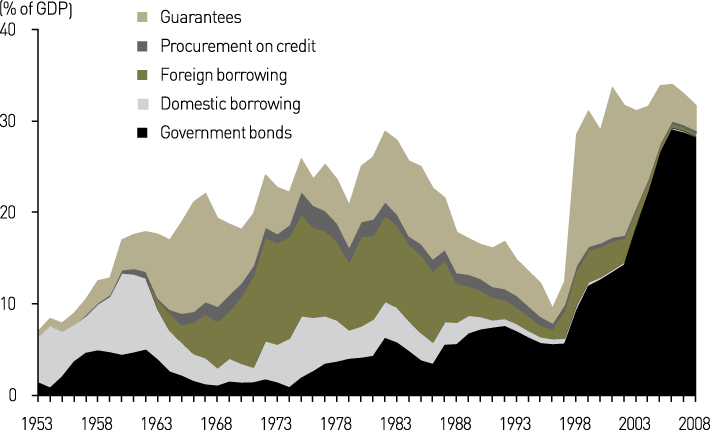

Fiscal consolidation also set public finances on a sustainable path. From the mid-1980s onward, the fiscal balance maintained a roughly stable position (Figure 2-10). Central government debt continued to decline and reached a very low level before the crisis (8 percent of GDP in 1996), which enabled the Korean government to address the 1997 financial crisis aggressively (Figure 2-11).

Fiscal consolidation, however, entailed costs in terms of lost output and increased unemployment. The unemployment rate jumped from 3.8 percent in 1979 to 5.2 percent in 1980, and then stayed at 4.0-4.5 percent before falling to 3.1 percent in 1987 and 2.5 percent in 1988 (Table 2-9). Fiscal consolidation appears to have prolonged the recession that began in 1980.

As mentioned above, monetary policy did not make a meaningful contribution to price stabilization.

Figure 2-10. Consolidated central government fiscal balance (1970-2009)

Figure 2-11. Central government debt (1953-2008)

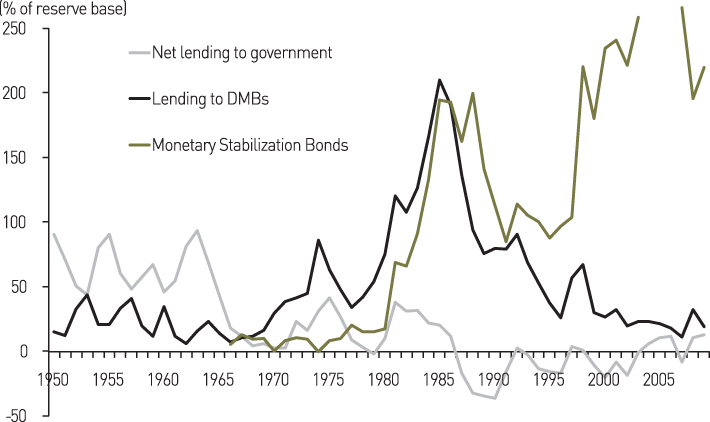

This was because of the continued existence of directed credits. The outstanding stock of central bank lending to DMBs exceeded 100 percent of the reserve base in 1981 and 200 percent in 1985, forcing the BOK to sell Monetary Stabilization Bonds (MSBs) to sterilize the increased reserves (Figure 2-12). This indicates that gearing monetary policy toward stabilization faced a fundamental difficulty as long as directed credits were continued.

Figure 2-12. Sterilization of central bank lending (1950-2009)

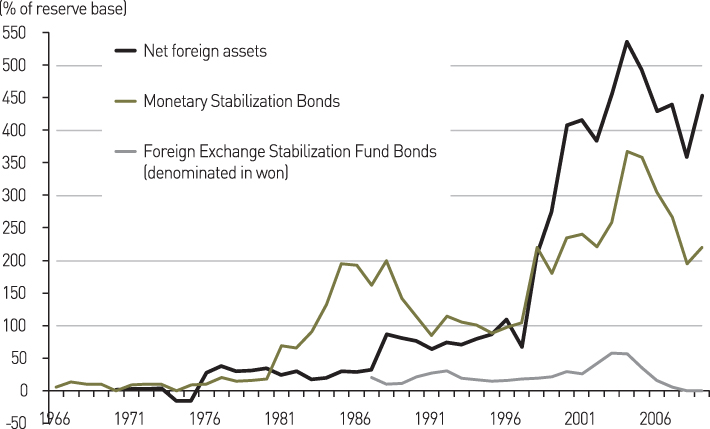

Another source of difficulty for the BOK was the increase in net foreign assets (NFAs).The latter increased to 87 percent of the reserve base at the end of 1988 (Figure 2-13). Alarge part of the current account surplus during the “three-low period” (1986-1988) was used to pay back foreign debts, and the rest showed up as increased NFAs on the BOK’s balance sheet. The government delayed exchange rate adjustment in order to sustain exports and encourage business investment, and started to revalue the won as late as 1988.

Japan and Taiwan, on the other hand, began their revaluation in September 1985 after the Plaza Accord was signed. The delay in revaluation is believed to have hampered efforts by businesses to enhance their competitiveness, retarded the restructuring of domestic industries, increased the stock of MSBs, and encouraged real estate speculation (Heung-ki Kim, 1999, p.344; Economic Planning Board, 1994, p.25).

Figure 2-13. Sterilization of net foreign assets (1966-2009)

As Figures 2-12 and 2-13 indicate, MSBs played avery important role in controlling money supply. In addition to MSBs, the BOK employed reserve requirement ratios and regulations on bank lending, but was not very successful in restraining money supply growth within annual targets. Out of 18 years between 1979 and 1996, targets were exceeded in 12 years. The large amount of interest payments on MSBs added to the money supply and caused the BOK big losses. The BOK wanted to minimize losses by forcing banks to buy MSBs at an interest rate below the market rate, their gap reaching 3percentage points at one point (OECD, 1994, p.113). This arrangement was discontinued in February 1997 with the introduction of a fully competitive auction system.

Source : SaKong, Il and Koh, Youngsun, 2010. The Korean Economy Six Decades of Growth and Development. Seoul: Korea Development Institute.

NOTE

1) The nominal exchange rate was kept at 484 won/dollar for 5 years between December 1974 and December 1979.

2) Jung-en Woo (1991, p.191) observes that these changes were led by economists at KDI and technocrats at EPB trained in the United States. Previously, most policymakers had been educated in the Japanese system and built their career in banks during the colonial period.

3) In ZBB, every spending item is examined thoroughly from top to bottom. In incremental budgeting, on the other hand, only increases in funding are examined in detail, taking the previous year’s funding as given. From this perspective, ZBB is nothing more than good budgeting practice, but proclaiming the adoption of ZBB for price stabilization must have had an “announcement” effect that facilitated the cooperation of ministries and politicians.

References

· Kim, Kwang Suk and Joon-kyung Kim,“ Korean Economic Development: An Overview,”in Dong- Se Cha and Kwang Suk Kim (eds.), The Korean Economy 1945-1995: Performance and Vision for the 21st Century, Korea Development Institute, 1995, pp.25-117 (in Korean).

· Kim, Heung-ki (ed.), Thirty-three Year History of the Economic Planning Board: Glory and Shame of the Korean Economy, Maeil Economic Daily, 1999 (in Korean).

· Kim, Heung-ki (ed.), Thirty-three Year History of the Economic Planning Board: Glory and Shame of the Korean Economy, Maeil Economic Daily, 1999 (in Korean).

· Thirty-year History of the Economic Planning Board Ⅱ (1981-1992): Economic Policies in the Liberalization Era, 1994 (in Korean).

· Kim, Heung-ki (ed.), Thirty-three Year History of the Economic Planning Board: Glory and Shame of the Korean Economy, Maeil Economic Daily, 1999 (in Korean).

· Thirty-year History of the Economic Planning Board Ⅱ (1981-1992): Economic Policies in the Liberalization Era, 1994 (in Korean).

· OECD Economic Surveys: Korea, 1994.

· Woo, Jung-en, Race to the Swift: State and Finance in Korean Industrialization, Columbia University Press, 1991.