As mentioned at the beginning of this chapter, one important policy goal of the Korean government has been the stabilization of real estate prices. Various government projects to build transportation networks, industrial parks and housing rapidly raised the land prices in targeted areas. The concentration of populations in large cities resulted in skyrocketing prices for residential and commercial properties. Property speculation became rampant.

Speculators, often from the well-to-do segment of the population, were blamed by the public for escalating real estate prices. Rising housing prices were of particular concern.

In response to the perceived increase in social inequality, the government introduced many measures to penalize speculative trading and curb windfall gains. For example, heavy taxes were levied on the capital gains from housing sales; home ownership was in principle allowed only to the actual residents of the home; and the renovation of high-rise apartments to create more units was restricted as it would result in capital gains for the existing owners. But these measures had an adverse impact on housing supply and hindered the smooth functioning of the property market.

More often than not, the government relaxed the regulations during recessions to boost the construction sector and stimulate the economy, and then tightened them again when worries about over-heating and speculation increased. Between the late 1960s and early 2008, the government announced a total of sixty-one measures, alternating between stimulus and stabilization packages.1) These short-term, “stop-go” policies increased uncertainties in the market and severely damaged the credibility of the government, fueling further speculation.

One notable innovation was the concept of “public stewardship toward land policy” adopted in the late 1980s. The government placed limits on the ownership of housing lots, imposed a tax on excessive profits earned from land sales, and introduced development charges. These policies were, however, ruled unconstitutional and abandoned in the 1990s.

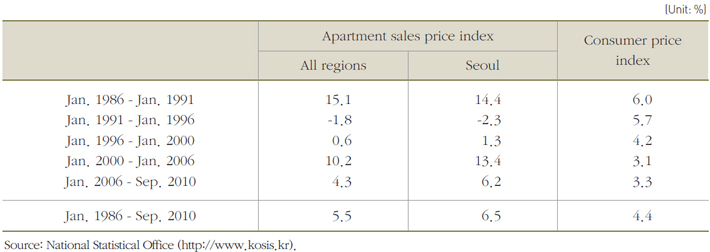

Amore successful strategy to stabilize housing prices was the large-scale housing construction project in the late 1980s. A target was set to supply 2 million units of housing in 1989-1992. The project was completed with the construction of 2.14 million houses (33 percent of the total housing stock of 6.45 million as of 1987) by August 1991, ahead of schedule. The housing supply ratio jumped from 69.2 percent in 1987 to 76.0 percent in 1992, and continued to rise to reach 93.3 percent in 1999. Between January 1991 and January 1996, the price index of apartment sales declined by 1.8 percent per year across the country and by 2.3 percent in Seoul (Table 5-9).

Table 5-9. Annualized growth rate of the price index for apartment sales

Entering the 2000s, housing prices began to rise again as the market recovered from the shock of the Asian financial crisis. The Roh Moo-hyun administration adopted measures on 13 separate occasions to curb housing speculation and asurge in prices, including the Real Estate Price Stabilization Measure announced in May 2003. Other measures included the requirement that the price of a home sale be reported to the authorities; the introduction of a comprehensive property tax with high rates; and more stringent rules on home loans, such as the loan-to-value ratio (LTV) and debt-to-income ratio (DTI) loan assessments.

Many believe that these measures to control demand, contrary to their stated goals, played a role in increasing housing prices in 2006 and 2007 as they reduced housing supply. Part of the measures were recognized for contributing to increased transparency in the housing market and promoting stability in the financial market, but a larger part signaled a departure from the market-based approach of the Kim Young-sam administration, which gave the private sector a leading role in housing supply.

At issue is the conceptual and practical difficulty of separating “speculation” from “genuine investment,” both of which are made in response to an expected rise in prices that increases the inflow of money into the sector and stimulates an increase in supply.

Past experience indicates that efforts to curb speculative demand can destabilize the housing market further and that the priority should be given to increasing housing supply, especially in regions suffering shortages (Man Cho, 2010).

Source : SaKong, Il and Koh, Youngsun, 2010. The Korean Economy Six Decades of Growth and Development. Seoul: Korea Development Institute.

NOTE

1) Examples include the real estate speculation prevention tax (currently the capital gains tax) introduced as a part of the Act on Special Measures for Preventing Real Estate Speculation in 1967; the tightening of regulations at the end of the 1970s, followed by easing in the early 1980s, tightening in the late 1980s, and easing once again at the end of the 1990s.