This article explores the key legislative and institutional transformations in South Korea's government accounting system from the immediate post-liberation period in 1945 through 2006. This history reflects a deliberate, decades-long journey to establish a sovereign fiscal framework, moving from inherited colonial-era structures and foreign military administration practices toward a more modern and domestically-led system. The evolution was marked by foundational legislation, significant organizational restructuring, and a persistent drive for greater efficiency and control in public finance.

#government accounting #public administration

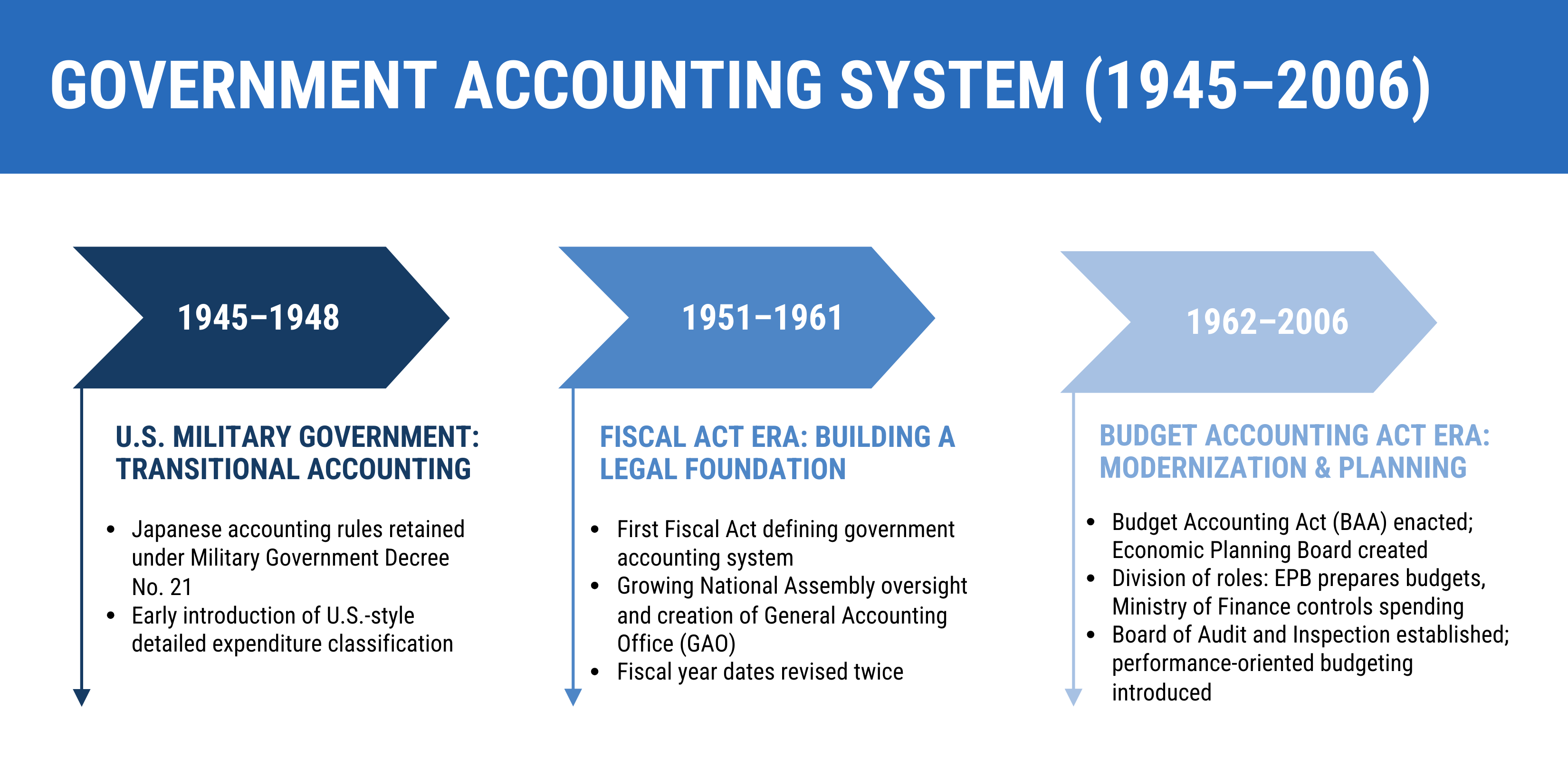

The years immediately following liberation were a critical transitional phase for South Korea's public administration. In the realm of government accounting, this period was characterized by the retention of existing systems alongside the selective introduction of new, American-influenced budgetary practices. This hybrid approach laid the groundwork for the future development of the nation's independent fiscal policies.

Following liberation, the U.S. Military Government largely maintained the existing administrative apparatus. Military Government Decree 21, issued in November 1945, stipulated that the accounting rules and standards of the Japanese Government-General of Korea would remain in effect, with the exception of allowing the government to set up and operate the Ministry of Finance if necessary.

However, the period was not merely one of preservation. The U.S. military's influence introduced significant changes to budgeting systems, creating a hybrid model. While the inherited Japanese accounting law featured a simple division of tax expenditures into "current cost" and "provisional cost," the U.S. military government implemented a more detailed approach. It required expenditures to be broken down into multiple specific accounts categorized by item and organization. As the historical record notes, the U.S. military government in Korea marked a transition period, in which the Japanese accounting law was retained for the most part, while elements of the American government’s accounting system were introduced in bits and parts. This dual system set the stage for South Korea's first independent fiscal legislation.

The enactment of the Fiscal Act in 1951 represented a foundational moment for the newly established republic. This legislation was the first comprehensive attempt to create a sovereign fiscal framework, establishing a legal basis for government accounting and budgeting. Although it drew heavily from foreign models, its passage was a critical step in building the nation's financial administrative capacity.

Passed in September 1951 and based on provisions in the 1948 Constitution, the Fiscal Act, effective as of October 1951, was the first-ever legislation that defined the system and rules of government accounting. The structure of the act emulated much of the Japanese Accounting Act (particularly in Chapters 1 and 3) and the Japanese Fiscal Act (particularly in Chapters 4 and the rest), both of which had been enacted in 1947.

Under this act, several key legal and institutional developments occurred. The fiscal year was amended twice: first in January 1954, moving the start date from April 1 to July 1, and again in June 1956, shifting it to January 1. More significantly, the act placed a growing emphasis on legislative oversight. It formally stressed the National Assembly’s role in monitoring administration and in drafting and settling budget accounts, granted the Minister of Finance authority over budget execution and settlement, and established the independent General Accounting Office (GAO) to review budget reports submitted to the legislature. These changes signaled an increasing effort to enhance control over the budgeting process.

Despite these significant structural reforms aimed at establishing formal control mechanisms, the act's ultimate impact on daily practice was limited. The source material concludes that the general awareness and standards of accounting remained unaltered for the most part. The shortcomings of this foundational but imperfect legislation created a clear need for a subsequent and more comprehensive legislative overhaul.

The Budget Accounting Act (BAA), enacted in December 1961, was a direct response to the shortcomings of its predecessor, which was not only a copy of Japanese legislation but had also revealed numerous practical flaws requiring a complete overhaul. It represented a major reform aimed at creating a more modern and efficient public finance system, driven by a new emphasis on centralized economic planning and performance.

This legislative overhaul was accompanied by significant organizational restructuring. In July 1961, the Government Organization Act was amended to create the powerful Economic Planning Board (EPB). The Budget Bureau was transferred from the Ministry of Finance to the new EPB, creating a clear division of labor: the EPB would oversee budget preparation, while the Ministry of Finance would control budget spending. An amendment of the Government Organization Act (GOA) in February 1966 led to the creation of the National Tax Service in March of the same year, further centralizing and professionalizing fiscal administration.

Oversight and auditing functions also evolved dramatically, reflecting the political shifts of the period. The General Accounting Office (GAO) was first established under Law 12 in December 1948. A critical amendment in September 1961 required the GAO to report to the Supreme Council for National Reconstruction (SCNR) instead of the President, a key indicator of the military government's centralization of power. The GAO was ultimately abolished following the enactment of the Board of Audit and Inspection Act in March 1963, with the new Board taking over the crucial responsibility of reviewing the government's accounting measures and practices.

The BAA introduced several key fiscal innovations intended to improve financial management. Most notably, the BAA introduced a performance-oriented budgeting system, shifting the focus toward results and efficiency. It also implemented other modernizing measures, such as setting aside appropriations for reserve funds and requiring the planned distribution of budgets to ensure more orderly and efficient management.

However, echoing a recurring theme in this historical progression, these formal modernizing efforts did not immediately transform the underlying administrative culture. The analysis from this period concludes that, even with these changes, the general awareness and standards of accounting remained unaltered for the most part. This era was thus a period of significant formal reform that successfully laid more of the essential groundwork for Korea's modern public finance system, even as practical application and cultural change lagged behind.