This article traces the institutional history of South Korea's national tax administration, examining its transformation across four distinct periods. From its initial formation in the turbulent years following independence to its current role as a modern, taxpayer-centric institution, the administration's evolution reflects the nation's broader journey of state-building, rapid economic development, and democratic maturation. By analyzing the key policies, organizational changes, and technological advancements of each era, we can understand how the system adapted to meet the changing needs of the state and its citizens.

#national tax service #tax administration #government

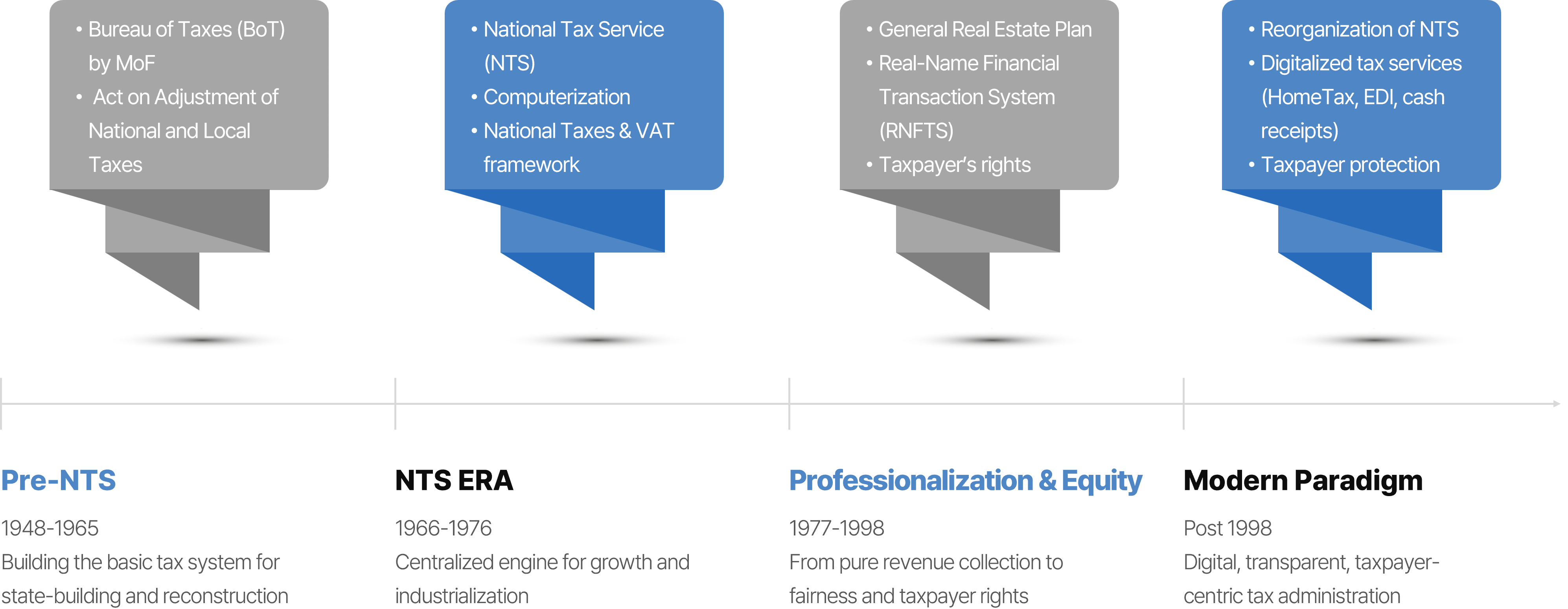

In the years following Korea's independence from colonial rule, establishing a coherent national tax system was a strategic imperative. Amidst the challenges of state formation and the devastation of the Korean War, building a stable revenue collection framework was a crucial prerequisite for economic reconstruction and future development planning. The efforts during this foundational period laid the essential groundwork for the centralized and powerful tax authority that would emerge. Initially, the finance bureaus of each province were responsible for levying and collecting local taxes. A nationwide structure began to take shape in March 1948 with the establishment of the Ministry of Finance's (MoF) Bureau of Taxes (BoT). This was established in conjunction with the creation of provincial tax departments and 64 local tax offices. However, the Korean War severely disrupted efforts to consolidate and stabilize this nascent system, even as new tax offices were opened to fund the war effort.

A significant shift occurred with the rise of the Park Chunghee administration and the launch of the First Five-Year Economic Development Plan in 1962. The government recognized that the existing tax administration, managed by the BoT within the MoF, was insufficient to secure the vast capital required for its ambitious industrialization agenda. The administration began to re-shape and consolidate the tax administration system in order to secure the massive amounts of capital and revenue needed for its industrialization drive. This administrative push included building human capital, evidenced by the MoF's creation of the Training Academy for Public Officials in 1962 to develop specialized expertise. The need for a separate, dedicated tax collection body became increasingly apparent, a view reinforced by the 1965 Nathan Report from the Economic Advisory Board. In response, President Park formed the Special Task Force for the Investigation of Tax Administration in September 1965 to review the nation's taxation status.

These foundational efforts and strategic reviews culminated in the decision to create a new, independent tax authority, setting the stage for a more centralized and aggressive approach to revenue collection.

The establishment of the National Tax Service (NTS) in 1966 marked a pivotal moment, transforming tax administration into a powerful engine for funding South Korea's rapid industrialization. This decade was characterized by the consolidation of a nationwide system designed for maximum efficiency in revenue collection, granting the new agency significant authority to meet the state's economic development goals.

The NTS officially came into being on March 3, 1966, with an initial structure of four bureaus, 13 offices, four local NTS branches, and 77 tax offices. The former Bureau of Taxes (BoT) was absorbed into the new structure and reorganized as the Bureau of the Taxation System. The impact on revenue collection was immediate and dramatic. In the year of its foundation, 1966, the NTS managed to collect KRW 70 billion in total in taxes, a 66.5 percent increase from 1965. This rapid growth continued with increases of 48.3 percent in 1967 and 50.5 percent in 1968.

The government's primary goals during this period were to reinforce and improve the science and efficiency of the tax administration system. Key initiatives supported this objective. The computerization of tax administration, which began in 1970 with the creation of the Office of Computerization, produced a staggering increase in processing capacity; the number of tax cases handled annually rose from approximately 4.5 million in 1965 to 15.6 million by 1969. The agency's investigative powers were strengthened with the addition of the Investigation Bureau in 1973, and the passage of the Framework Act on National Taxes in 1974 provided a clear legal foundation for tax administration. Tax policy also evolved, with the expansion of the general income tax system in 1975 and legislative changes in 1976 that established the basic framework for the Value-Added Tax (VAT). While these measures were crucial for securing revenue for economic development, the drive for efficiency had consequences. In pursuing this aim, however, tax administration came to take on compulsive aspects.

This period firmly established the NTS as a formidable state institution, whose successes in revenue collection directly fueled the nation's economic miracle and paved the way for the system's subsequent professionalization.

As the South Korean economy entered a phase of maturity and increased globalization, the focus of national tax administration shifted from pure revenue maximization to achieving greater stability, equity, and technological sophistication. This two-decade period was marked by a drive to professionalize the system, making it fairer and more responsive to both domestic economic conditions and international trends.

Equity and fairness emerged as central policy themes. Major initiatives were introduced to address economic imbalances, particularly in the real estate market. The General Real Estate Plan (GREP) of 1988 raised the transfer income tax to curb speculation. The landmark implementation of the Real-Name Financial Transaction System (RNFTS) in 1993 was a critical step toward financial transparency. The tax system was further refined with a major overhaul of the Act on the Regulation of Tax Reduction and Exemption in 1981 to improve the neutrality of tax benefits.

Significant technological and organizational advancements paralleled these policy shifts. The push to computerize tax administration made steady progress throughout the period. The Tax Integration System (TIS) was launched in 1997, epitomizing the rapidly advancing state of science and professionalism in tax administration. As Korea’s integration into the global economy deepened, the administration made direct organizational responses to the growing volume of international tax matters. This included creating the Bureau of International Taxation in 1986, dispatching tax liaison officers overseas, and establishing the high-level position of International Tax Coordination Officer in 1987.

This era also saw a notable evolution in the relationship between the administration and the public. "Trust, friendliness, and service" became keywords, reflecting a growing societal perception of the taxpayer as an autonomous actor. This shift culminated in the 1997 Declaration of Taxpayers’ Rights, which formally acknowledged this new relationship. This formal acknowledgment of the taxpayer's role would soon be tested and accelerated by the profound institutional reforms demanded in the wake of the 1997 Foreign Exchange Crisis.

The 1997 Foreign Exchange Crisis served as a powerful catalyst for profound reforms across South Korean society, including its national tax administration. The subsequent Kim Daejung administration responded to soaring public demand for social reform by prioritizing the transparency and efficiency of government functions. This created the impetus for a fundamental paradigm shift in tax administration, reorienting the entire system around taxpayer service and convenience.

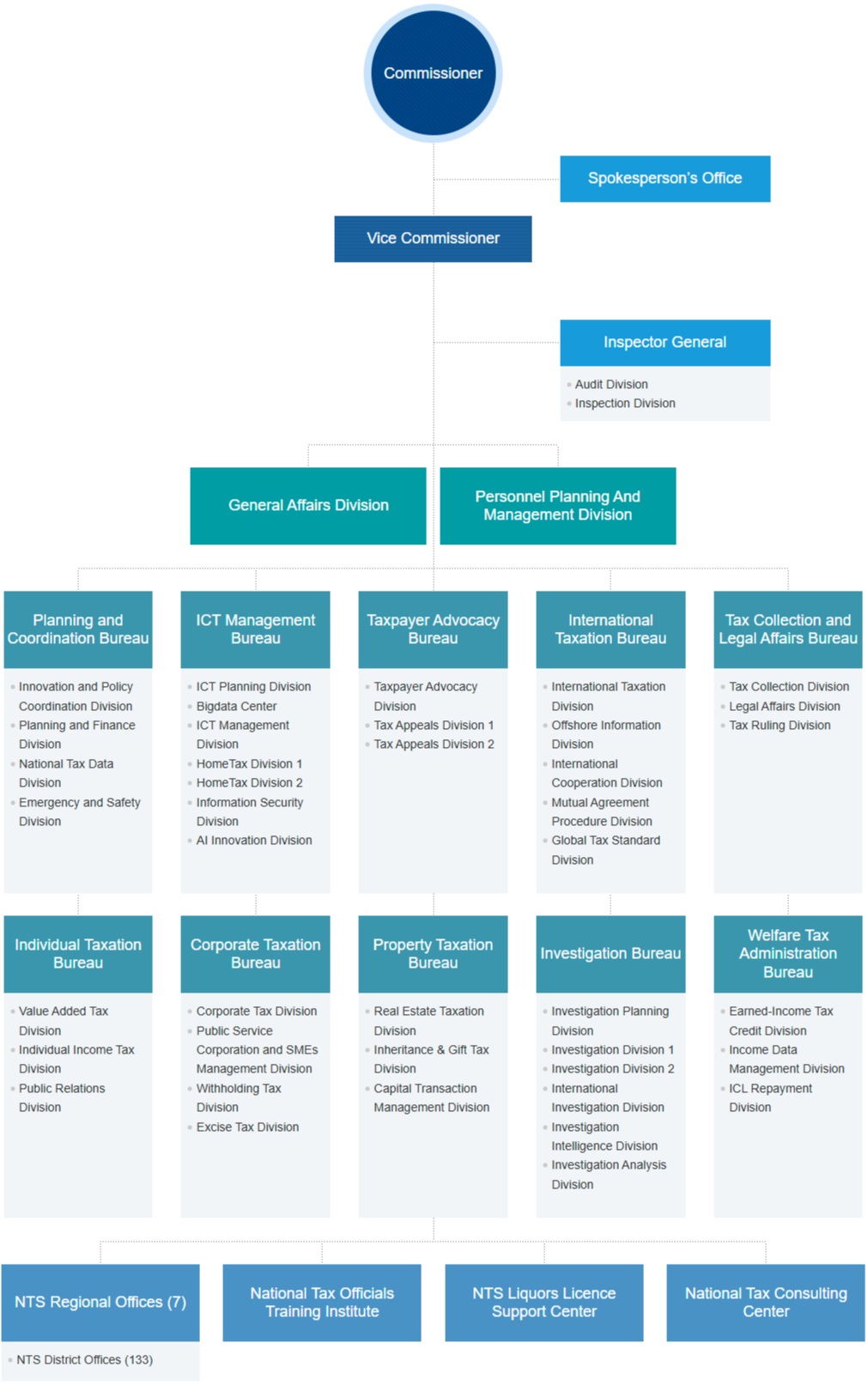

Sweeping organizational reforms were implemented in 1999. In a key administrative move, the NTS was reorganized by function, with the headquarters specializing in planning, local branches in investigation, and tax offices in taxpayer services. This restructuring included the closure of one local branch and the merger of 35 offices. The resources saved were reinvested directly into improving taxpayer services, exemplified by the establishment of the Bureau of Taxpayer Support. This functional separation was a strategic response designed to minimize direct contact between tax officials and taxpayers, which, as a result, drastically reduced tax-related complaints.

This period also witnessed rapid advancements in automation and computerization. The electronic data interchange (EDI) system was established in 1998 to enable online tax payments. A national administration intranet was launched in 1999, dramatically improving internal efficiency. The introduction of the Home Tax Service in 2001 was a landmark achievement, bringing most taxation tasks online and fundamentally transforming service delivery for the public.

These reforms represented more than just organizational and technological upgrades; they signified a new philosophy. The keywords of the era—"taxpayer," "the people," and "taxpayers’ convenience"—highlighted a new relationship between the state and its citizens. These keywords reflect the growing social awareness that taxpayers were no longer to be treated as mere passive objects of tax administration, but as autonomous and active participants in the tax administration system.

This historical journey reveals the transformation of South Korea's tax administration from a basic tool for state-building and industrial financing into a sophisticated, modern, and service-oriented institution.